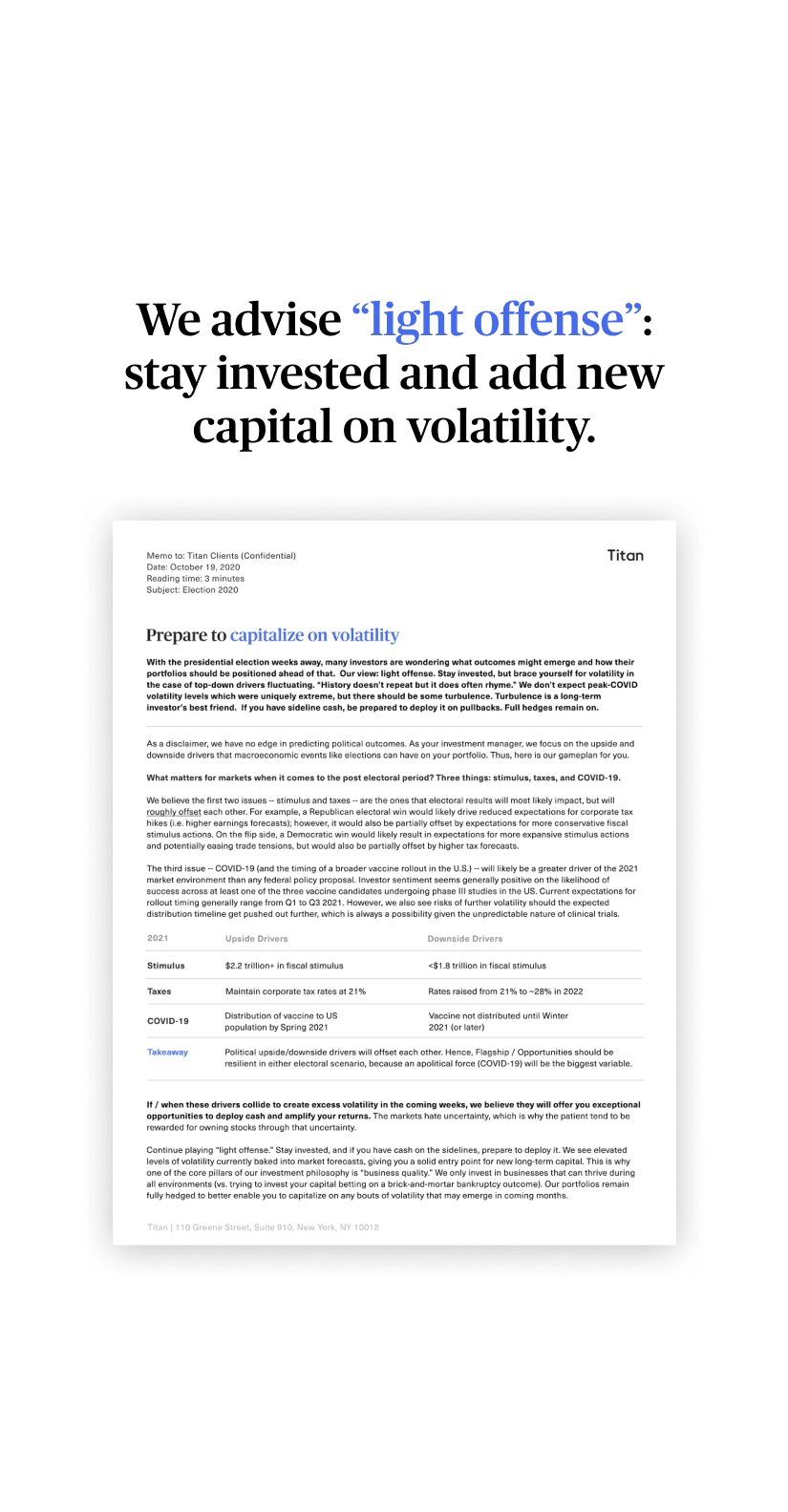

Go all in? Not yet.

Apr 16, 2020

After this 25% rally from March lows, we’re shifting our tone from aggressive offense (“go time” is what we called it) to light offense. By our rough estimates, the market at these levels now has 45% upside and 35% downside through year end. These are roughly “even odds,” or a 1:1 skew vs. the 3:1 skew we saw in mid-March.

While we are inherently optimistic as growth investors, we believe some are too optimistic about the speed of a COVID-19 recovery. We see real probabilities that a pullback could occur in the coming months as the world comes out of quarantine. Short-term even odds coupled with long-term excellent odds equals light offense. Spread out your buys; keep some excess cash ready to deploy.

Attached is our full memo and a 10-min audio summary from our Co-CEOs.

Agenda for audio note:

0:40 - What's changed over the past month 1:35 - Our variant perception today 2:30 - Why COVID-19 is misunderstood 3:30 - Why we're still net optimists 4:50 - When we'd shift to aggressive offense 5:55 - Prospective returns for Titan stocks 6:50 - Examples of Titan stocks poised to 2x 8:00 - What we're least confident about 8:55 - Any changes to our Flagship strategy?

Back in March, we signaled “go time” to our clients, flagging the opportunity to buy:

"Everyone is fearful. Markets are reflexively capitulating on that fear, down nearly 25% this year. The time to be greedy is near. Go time approaches... Many stocks now sell for what we believe are fire sale prices." (March 13th, Titan Research)

"We think it's "go time" for long-term investors. We don't know when a bottom will come, but it will, and our durable portfolio of companies is selling for extremely attractive valuations for long-term investors." (March 24th, Titan Research)

Little did we know, we nearly called the bottom (March 23rd). Do not give us credit for timing the market. This was pure luck as frankly the market could have fallen further. What we did do was ascertain price vs. value. Google at $1,050 a share, Uber at $15, FB at $150 were absolute bargain prices vs. our view of intrinsic value, implying 20%+ annualized returns on some of the best business models mankind has ever seen. Even if the market fell further, they were prices one would not regret. It would have been nitpicking to wait further.

Since then, the market has rallied +25% without any meaningful new data on this COVID-19 fight, aside from massive monetary and fiscal stimulus. Because of this rally in spite of risks remaining, our view has shifted from aggressive offense to light offense. We suspect, but cannot predict, that you’ll have another pullback to buy at an even better upside/downside skew.

Right now, optimists on CNBC are screaming to “buy the dip,” pointing to improving COVID-19 data, unprecedented stimulus, and stocks still 15% below the Feb highs.

"Unlikely to make new lows" - Goldman Sachs "Bear market has concluded" - Piper Sandler "All-time highs next year" - JPMorgan Chase

While they are right that the market could have significant upside, they don’t appropriately weigh the probability of the downside. These include (but are not limited to) social distancing not being as effective as modeled, having to re-quarantine again in the fall, and “herd immunity” being much further away than estimated. As growth investors at Titan, we’re also natural optimists - we think the world will recover and the 2020s will roar again. Ascribing a near-100% probability to a 6 month recovery, however, seems a bit foolish in our opinion.

Should you be selling (defense)? No. Your Flagship holdings are still well off their previous highs despite minimal impact to long-term earnings power, which means there is significant upside. Several of them should actually exit this crisis stronger (e.g., Netflix, Amazon) as sub-scale competitors close up shop.

Should you be going all-in now (extreme offense)? No. Investing is about betting big when the risk/reward is favorable. Right now, it’s even (1:1). If the market falls 25%, you’d have upside of 90% and downside of 30%, leading to an up/down ratio of 3:1... this is roughly when we’d say to restart aggressive offense. This is the type of skew that you hunt for on a single company basis. If the entire market offered this skew, it would be a wonderful time to be a buyer.

We hope by all means we are wrong, that COVID-19 disappears faster than expected, and this skew never comes back. But the risks unfortunately remain and as investors that means spreading out buying while also staying patient for future opportunities. Today’s prices are good, but they could become wonderful again. If you have cash sitting around, hold some as dry powder ready to strike. We call this light offense.

In our attached memo, on page 2, you’ll see how we think about the potential risk/reward skew for U.S. equities in the short-term. We completely understand that volatility can be tough to stomach at times, but now is a critical moment to remain level-headed, data-driven, and patient with your capital.

“Calm seas never made a skilled sailor.”

Let us know if you have any questions, Titan Research

Cash Management

© Copyright 2024 Titan Global Capital Management USA LLC. All Rights Reserved.

Titan Global Capital Management USA LLC ("Titan") is an investment adviser registered with the Securities and Exchange Commission (“SEC”). By using this website, you accept and agree to Titan’s Terms of Use and Privacy Policy. Titan’s investment advisory services are available only to residents of the United States in jurisdictions where Titan is registered. Nothing on this website should be considered an offer, solicitation of an offer, or advice to buy or sell securities or investment products. Past performance is no guarantee of future results. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Account holdings and other information provided are for illustrative purposes only and are not to be considered investment recommendations. The content on this website is for informational purposes only and does not constitute a comprehensive description of Titan’s investment advisory services.

Please refer to Titan's Program Brochure for important additional information. Certain investments are not suitable for all investors. Before investing, you should consider your investment objectives and any fees charged by Titan. The rate of return on investments can vary widely over time, especially for long term investments. Investment losses are possible, including the potential loss of all amounts invested, including principal. Brokerage services are provided to Titan Clients by Titan Global Technologies LLC and Apex Clearing Corporation, both registered broker-dealers and members of FINRA/SIPC. For more information, visit our disclosures page. You may check the background of these firms by visiting FINRA's BrokerCheck.

Various Registered Investment Company products (“Third Party Funds”) offered by third party fund families and investment companies are made available on the platform. Some of these Third Party Funds are offered through Titan Global Technologies LLC. Other Third Party Funds are offered to advisory clients by Titan. Before investing in such Third Party Funds you should consult the specific supplemental information available for each product. Please refer to Titan's Program Brochure for important additional information. Certain Third Party Funds that are available on Titan’s platform are interval funds. Investments in interval funds are highly speculative and subject to a lack of liquidity that is generally available in other types of investments. Actual investment return and principal value is likely to fluctuate and may depreciate in value when redeemed. Liquidity and distributions are not guaranteed, and are subject to availability at the discretion of the Third Party Fund.

The cash sweep program is made available in coordination with Apex Clearing Corporation through Titan Global Technologies LLC. Please visit www.titan.com/legal for applicable terms and conditions and important disclosures.

Cryptocurrency advisory services are provided by Titan.

Information provided by Titan Support is for informational and general educational purposes only and is not investment or financial advice.

Contact Titan at support@titan.com. 508 LaGuardia Place NY, NY 10012.