You're successful. You're saving. But something doesn't feel right.

Maybe it's the four different 401(k)s from past employers collecting dust. The random brokerage accounts you opened during 2020-2021. The crypto wallets whose passwords you can barely remember. And that persistent feeling that you're missing opportunities because you simply can't see the full picture.

Sound familiar? I hear this every day from people just like you.

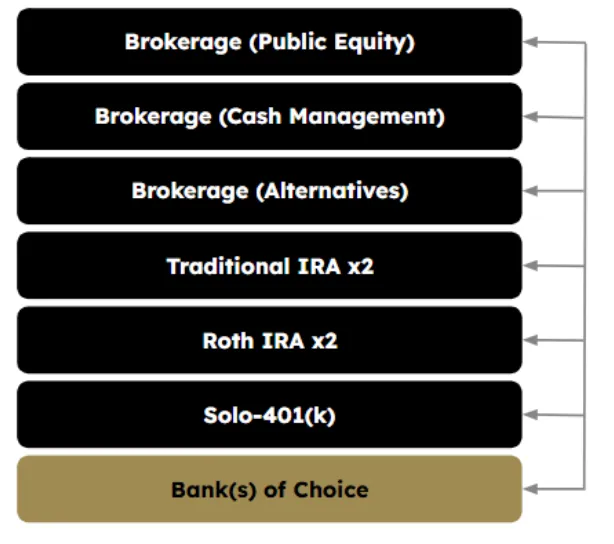

Imagine going from the above, to something like this:

Just last week, a client told me:

"I have my current 401k, a rollover IRA, my wife has a current 401k and then a rollover IRA. I get my RSUs through a different platform... the number of accounts is starting to get into double digits."

This scattered approach isn't just annoying when tax season rolls around—it can quietly undermine your ability to build wealth over time:

- You may not have a coherent investment strategy (just a collection of accounts)

- You're likely holding overlapping positions you can't easily track

- You could be missing crucial rebalancing opportunities

- You could be creating tax inefficiencies you don't even know about

- And let's be honest—you probably have forgotten accounts somewhere

The Real Cost of Financial Fragmentation

1. Death by a Thousand Fees

The cost of scattered accounts goes beyond inconvenience. From our client conversations, we typically see:

- Legacy Account Fees: Moving from 0.8% to 0.2% in management fees after consolidation

- Hidden Costs: Many clients discover they're paying multiple layers of fees across different platforms

- Service Overlap: One client had accounts spread across E-Trade, Morgan Stanley, Fidelity, and T. Rowe Price, each with their own fee structures

2. Tax Inefficiency Costs

This is where the real money disappears:

- Lost Tax Alpha: Strategic consolidation generates around 2% annually in tax alpha through proper positioning.

- Daily Optimization: Consolidated accounts allow for daily rate scans to optimize the highest after-tax yield possible.

- Harvesting Opportunities: Create a reserve of tax losses that can offset future gains.

The Numbers Add Up Fast

For a typical tech professional, here's what consolidation achieves:

- Fee Reduction: Real client example showing reduction from 0.7% to 0.29% in total fees

- Tax Efficiency: Clients gain approximately 2% annually in tax alpha through strategic positioning

- Professional Services: Average savings of $600 annually just in CPA fees

Real Client Example

Consider this tech professional who came to us with:

- Multiple 401(k)s from past employers

- RSUs through different platforms

- Various brokerage accounts

- Account reaching double digits

After implementing our consolidation strategy:

- Fee Structure: Reduced from 0.7% to 0.29% on the consolidated portfolio

- Tax Optimization: Implemented daily rate scans for highest after-tax yield on cash

- Strategic Benefits: Created a tax-loss harvesting system to offset future gains

- Operational Efficiency: Created one centralized home base for all investment accounts

The result? A structure that's sustainable, with significant annual savings through lower fees, better tax efficiency, and simplified management.

Why Smart People End Up Here

If you're wondering how you ended up in this situation despite being financially savvy, you're not alone. Here are a few patterns I typically see:

Career Transitions: Clients often say things like, "I've been a contractor for a long time. So I've had various 401ks and SEP IRAs across all the previous companies I’ve worked for.”

Chasing The Promos: Clients often describe situations like, "Robinhood is offering this, so then I'll just transfer money into there... They end up having a lot of duplicative strategies." (Did you also open that Coinbase account in 2021?)

Paralysis by Analysis: Clients often mention something like, "I spend... a couple of hours each of those days, looking at all my accounts, thinking about it. Where is the allocation off?" How many weekend hours have you lost to this exact activity?

The Framework for Financial Clarity

It really comes down to defining a game plan: (i) here’s where we are (ii) here’s where we’re going, and most importantly (iii) here’s how we’re going to get there.

Step 1: Get the Full Picture

First, we need to understand what you actually own. As I tell my clients: let’s start by taking a look at all your statements and summarizing what you already own.

You'd be surprised how many tech professionals I work with who discover they're nearly 80% in tech stocks when we lay everything out—not exactly the diversification they thought they had.

Step 2: Identify Inefficiencies

Next, we'll look for the hidden problems:

- Those overlapping ETFs (you're duplicating your exposure to the same underlying investments)

- The legacy accounts still charging you 1990s-era fees (often significantly higher than typical fees seen today)

- The tax bombs waiting to happen in the wrong account types

- The concentration risks you didn't realize were building up

- The tax-advantaged accounts you're not maximizing

Step 3: Strategic Consolidation

Not all consolidation is equal. Together, we'll:

- Execute any beneficial rollovers designed to avoid unnecessary taxes

- Maintain strategic positions when it makes sense

- Put the appropriate investments in the right account types

- Help preserve those valuable tax advantages you've earned

Step 4: Create a Forward-Looking Strategy

As one client perfectly put it: "The idea would be to just say, look, I don't want to have six different accounts as I change jobs and move on to the next gig. It's nice to have one centralized home base that I'm confident in."

This isn't just about cleaning up the past—it's about setting up a system that makes your financial future clearer, more manageable, and potentially more profitable.

Beyond the Direct Savings

The benefits extend far beyond just fees and taxes:

- Better Risk Management: Access to professional investment management with a .2% AUM fee.

- Proactive Tax Planning: Optimizing your cash for the highest anticipated after-tax yield in Smart Treasury based on your customized tax information.

- Strategic Opportunities: We aim to reduce costs by up to 25 basis points from day one... and even small improvements like that may compounds over time.

Common Concerns Addressed

"Won't I lose something in consolidation?"

Not necessarily. Direct rollovers are generally non-taxable events. This means that when you rollover directly from one financial institution to another, even if that means selling all the securities in the account being rolled over, no tax liability is realized.

"What about my company 401(k)?"

While you typically can't roll over an active 401(k), we can help evaluate whether it's optimized within your broader strategy. No account left behind.

"I have positions I don't want to sell"

We can often work around existing positions: Your strategy should work for you, not the other way around.

What Smart Consolidation Looks Like

Here's what I do for clients every day:

- Analyze Current Costs: We take a look at your accounts, provide insights, and put together a more holistic plan for all of your investible assets, including an analysis of the fees you are paying.

- Strategic Transfers: We take on the heavy lifting of any transfers, all you have to do is provide us with your account statements.

- Tax-Efficient Transitions: We optimize the transfer of securities according to your goals.

Your Next Steps

- Get Organized: Take 20 minutes to list all your investment accounts (yes, even that Robinhood account you haven't looked at since 2021)

- Book a Free Consultation: Let's review your full picture together

- Create Your Plan: We'll help design a clear path forward that makes sense for your unique situation

Remember: The goal isn't just consolidation—it's creating clarity and confidence in your financial future. It's about having the mental bandwidth to focus on the things that matter most to you. And yes, it's about potentially saving up to thousands of dollars every year that may quietly be leaking from your accounts right now.

Ready to bring order to your financial life? Schedule a free consultation with one of our advisors who works with tech professionals like you to consolidate and optimize their investments.